Defining The Disruptive Geopolitics Of The Global Farms Race

June 18th, 2009

Via The Market Oracle, an interesting investment-focused review of the global land grab. As the article notes:

“…According to the Economist, Saudi Arabia, Kuwait, and China have been “quietly” buying up more than $20 billion of this asset.

It’s not oil or natural gas assets though. And it’s not the molybdenum they need to build thousands of miles of new pipelines. They’re buying up one of my favorite long-term investments, farmland.

The way things are shaping up, investors who follow their lead now will do exceptionally well in the short-term and long-term. Let me explain.

Another Case of Great Expecations

It’s no secret we’re facing a big opportunity in agriculture. It’s something we’ve delved into quite a bit over the past few years.

Still though, there are a lot of people who haven’t “bought in” to the opportunity here. The thing most investors still fail to understand about agriculture is last year’s credit crunch is a good thing. I expect it to go a long way to making a great opportunity even better.

Right now, official estimates for this year’s crop are far too optimistic. Currently, the U.S. Department of Agriculture (USDA) expects world grain production to rise 4.9% this year. And they’re expecting an increase of 3.1% in 2010.

Granted, that sounds reasonable to most people. But they’re not reasonable expectations at all.

You see, these are very rosy expectations for so many reasons. First, you have to consider that 2008 was one of the top three crop production years in history. The sharp rise in crop prices over the past few years sent farmers around the world into full production mode. The past two years were exceptional. Even though, demand still outstripped supply and food riots broke out around the world.

Also, agriculture production doesn’t grow that fast. It grows at a snail’s pace. An average year will see about 1% to 2% growth – maximum. The past few years have been an exception, not the norm.

The final thing the USDA is missing is agriculture production goes hand in hand with the economy. According to a recent report by Credit Suisse, “[2009] would be the first global recession to coincide with increased crop production.”

So the USDA growth estimates are downright laughable. That’s good news for us though. The misguided USDA is helping keep the window of opportunity open. And when we look through that window, we can see a very big opportunity.

It’s All Relative

The agriculture boom has a lot more room to run than most people realize.

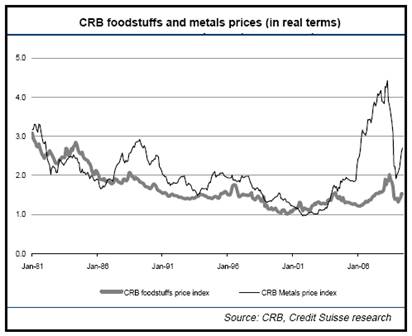

A research report from Credit Suisse– released earlier this week shows how much higher agriculture prices realistically could go. The chart below, excerpted from the bank’s report explains it all.

The chart shows the Commodity Research Bureau (CRB) foodstuffs price index (bold line) relative to the CRB metals index (thin line) over the past 28 years in real (inflation-adjusted) terms.

As you can see, there is a lot more upside left for agriculture. And that’s despite the great run agriculture has had over the past few years, the correction during the credit crisis, and rally going on now.

For instance, metals prices soared between 2002 and 2008. The CRB metals index more than quadrupled. Needless to say, they were hot. But agriculture, only caught on near the end of the rally.

Basically, the chart shows food prices have a lot more room to run. If food prices only return to their inflation-adjusted highs of the early 1980’s, they’re double from here. If they climb as high as metals did, they could triple.

The biggest gains won’t be had in agriculture commodities like wheat, corn and soybeans though. They’ll be in the producers of those commodities. And when it comes to agriculture, the only producer is farmland.

Leveraging Up on Agriculture

The secret to making a fortune in commodities is leverage. Just take a look at what has happened over the past few years. Gold prices have quadrupled, but dozens of gold mining stocks (even the larger ones) have watched their shares climb 1,000% or more.

The same is true for silver, copper, zinc, and most other metals. The underlying metal price climbs and the miners of those metals absolutely soar.

Miners, as the producers of metals, always offer more leverage.

The same is true for farmland. But there’s something unique about farmland which offers much more upside than mining stocks that performed exceptionally well during the metals boom.

In mining, when commodity prices rise, a global land grab ensues. The big money sees profit opportunity and billions of dollars start flowing into exploration and mine development projects to open new mines. During the last metal boom, dozens of new mines opened up.

It’s simple economics. Demand goes up. Prices go up. Eventually supply catches up to meet demand. It works on the way up and the way down.

That’s mining though. There are a lot of potential mines out there. When it comes to farmland though, there isn’t much more farmland left in the world.

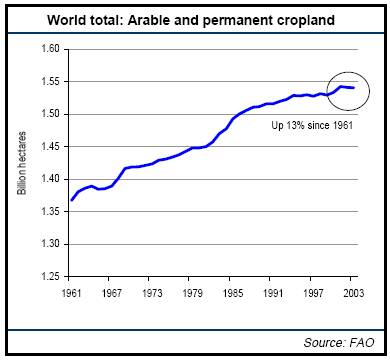

As the chart below shows, the world has practically reached “Peak Soil.”

As you can see, the amount of new farmland created over the past 48 years is tiny. The total increase in arable and permanent cropland has been a paltry 13%. That’s an annual expansion rate of 0.27% per year.

Whether the farmland was created by tearing down rain forests, converting pasture to crop producing land, or using technologically advanced seeds, chemical fertilizers, and irrigation to turn marginal farmland into more productive, the world is running out of ways to create more farmland.

We’ve reached Peak Soil.

Of course, there are other considerations here. The introduction and improvement of genetically modified organics (GMO) have gone a long way to increasing crop yields from the finite soil, but the gains in productivity from here will be limited. Soil quality is declining and those banner years of crop production will start to plateau.

Of course, there are two questions which have to be answered before putting your investments dollars to work. First, we have to figure out where. In this case, farmland offers a lot. Second, we have to figure out when. The way things are shaping up, the time is now.

Hitting Paydirt

The credit crunch has been hard on a lot of people. Unemployment continues to rise around the world. Manufacturing activity is down. The economy, despite showing some signs of turning around (which will be short-lived – less than two years), is still in decline.

It has been tough on everyone – including farmers. The value of farmland has fallen drastically around the world when valued in U.S. dollars according to the Economist.

In the past year, the only major crop producing to see the value of its farmland rise is in the United States. Everywhere else is showing a completely different picture.

Farmland prices are off 12% in the Canadian prairies. They’re down nearly 18%% in Brazil. In Russia and Bulgaria, farmland has dropped anywhere from 20% to 35% depending on the region.

The biggest drop, however, had been in Ukraine. Farmland prices have plummeted more than 70%. The price of Ukraine’s fertile acres has been hit hard for two reasons. First, the overall decline in global farmland values has impacted Ukraine. Second, the combination of political instability and a law preventing ownership of farmland (it’s only available for lease – even though those leases can run 30 to 60 years).

The combination of a tremendous upside combined with an industry that is still feeling the pain from the recession, overly optimistic expectations for this year’s worldwide harvest, and the upside potential make farmland a very attractive place to buy right now.

Remember, investing is all about risk and reward. Right now the risk of a decline in farmland is small and the upside, well…if crop prices only double, you’ll see farmland values soar higher and faster.

So if you’re looking to put some “safe” money to work, in a sector which has fallen out of favor, and one which is facing a secular growth trend which has years ahead of it (what we’re always looking for at the Prosperity Dispatch), right now farmland is definitely worth a look.

The big money in Saudi Arabia, Kuwait, and China are getting on board. Maybe you should too.

This entry was posted on Thursday, June 18th, 2009 at 9:59 am and is filed under Uncategorized. You can follow any responses to this entry through the RSS 2.0 feed. You can leave a response, or trackback from your own site.

Leave a Reply

Warning: Undefined variable $user_ID in /home/sysadmin/domains/seedsofarevolution.com/public_html/wp-content/themes/seedsofarevolution/comments.php on line 68

You must be logged in to post a comment.

Educated at Yale University (Bachelor of Arts - History) and Harvard (Master in Public Policy - International Development), Monty Simus has long held a keen interest in natural resource policy and the geopolitical implications of anticipated stresses in the areas of freshwater scarcity, biodiversity reserves & parks, and farm land. Monty has lived, worked, and traveled in more than forty countries spanning Africa, China, western Europe, the Middle East, South America, and Southeast & Central Asia, and his personal interests comprise economic development, policy, investment, technology, natural resources, and the environment, with a particular focus on globalization’s impact upon these subject areas. Monty writes about freshwater scarcity issues at www.waterpolitics.com and frontier investment markets at www.wildcatsandblacksheep.com.